Take This Job and Shove It: Why the job market gave the Fed cover to cut rates

When country songs describe economic conditions perfectly

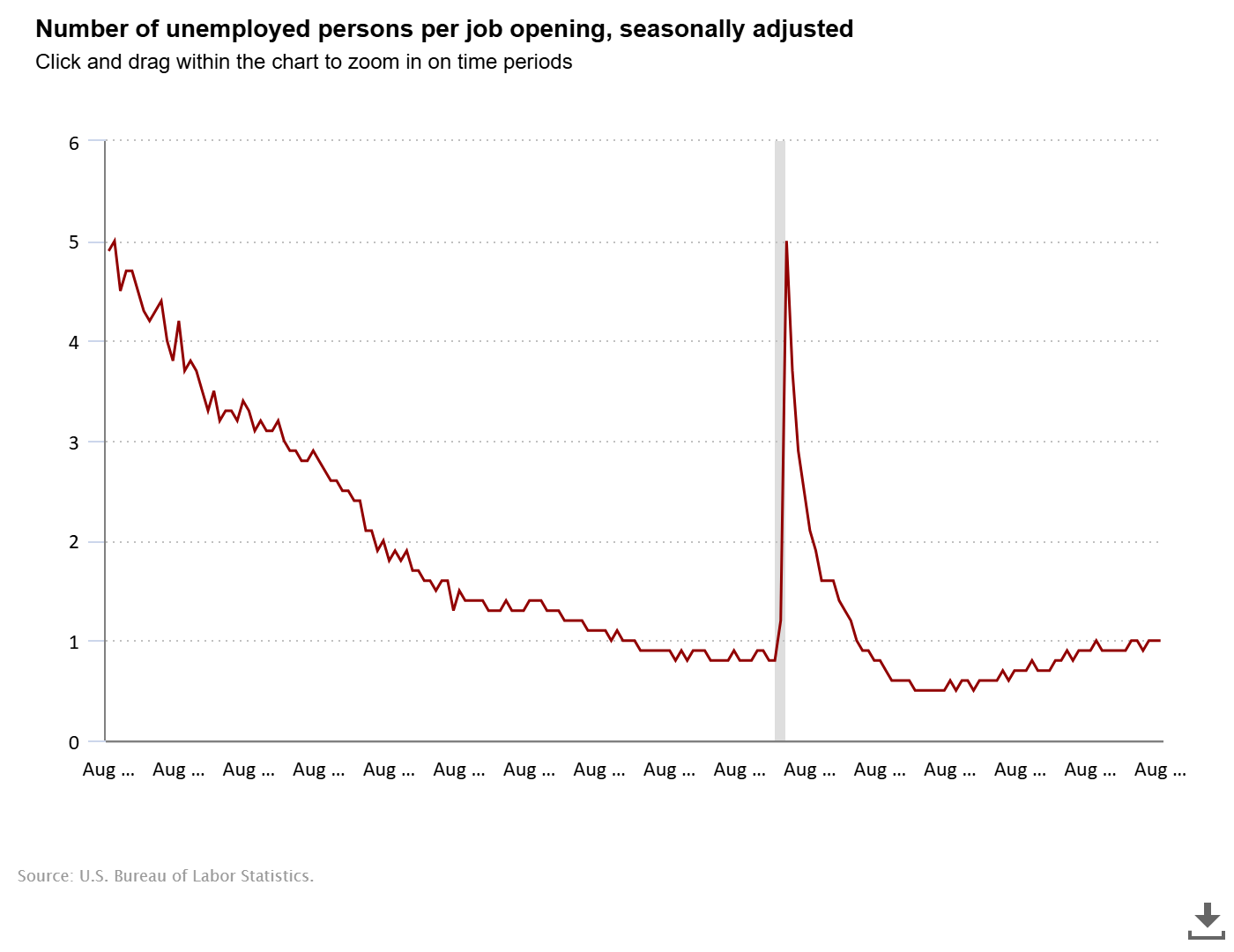

Shaded area represents recession, as determined by the National Bureau of Economic Research

The U.S. economy maintained a path of robust yet moderated growth throughout the third quarter of 2025, though beneath the surface, monetary policy underwent a critical pivot. Preliminary estimates suggested that U.S. GDP growth was tracking solidly, with some nowcasts indicating annualized growth potentially as high as 3.9% . This growth occurred despite a major policy shift by the Federal Reserve, which executed its first interest rate cut of the year in September. The central bank lowered the target range for the Federal Funds Rate to 4.0%–4.25%, signaling an intent to balance persistent, tariff-induced inflation risks with clear evidence of a cooling labor market. This shift in policy reassured markets that the Fed was prepared to support the economic expansion.

The cooling of the labor market was perhaps the most compelling economic signal of the quarter and a primary justification for the Fed’s pivot. The unemployment rate ticked up in August, and monthly non-farm payroll additions slowed significantly, pointing toward a decisive moderation in wage and employment pressure. Commodity markets delivered highly mixed quarter-to-date results: precious metals were the clear standout, with gold surging to a record high per ounce, driven by safe-haven demand amid geopolitical tensions and the prospect of lower real rates. Conversely, ample supply and reduced global demand kept the broad energy sector range-bound, resulting in crude oil prices registering a slight net decline for the quarter.

Overall, the combination of resilient corporate performance and the perceived benefit of monetary easing drove the U.S. stock market higher. The S&P 500 Index delivered a strong quarter-to-date gain of approximately 8.12%, pushing the index near its all-time highs as of the end of September and the MSCI ACWI was up approximately 7.5%. Investor sentiment was bolstered by positive earnings guidance, with estimated year-over-year earnings growth for the S&P 500 tracking at approximately. Technology, Materials, and Financials were particularly strong performers, suggesting that corporate fundamentals remained solid despite trade policy uncertainty. Focus now turns to the fourth quarter, with expectations of further rate cuts hinging entirely on the continued trajectory of the jobs market and inflation.

###

Harbor Ridge Investments (“Harbor Ridge”) is a specialty division of Reflection Asset Management (“RAM”), which is an investment adviser registered with the Securities and Exchange Commission (“SEC”) under the Investment Advisers Act of 1940. SEC registration does not constitute an endorsement of the firm by the Commission, nor does it indicate that the adviser or investment adviser representative has attained a particular level of skill or ability.

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed, and Harbor Ridge makes no representation or warranty as to the accuracy or completeness of the information, which should not be used as the basis of any investment decision. Information contained on third party websites that Harbor Ridge may link to is not reviewed in their entirety for accuracy and Harbor Ridge assumes no liability for the information contained on these websites. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of writing and are subject to change without notice. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from Harbor Ridge Investments. For more information about Harbor Ridge Investments, including our Form ADV brochures, please visit https://adviserinfo.sec.gov or contact us at bmoszeter@harborridgeinv.com.